Insights

5

min read

Where Is The Telecommunications Industry’s AI Maturity?

Artificial intelligence has become the central theme in the transformation of global telecom operators. Shareholders expect telcos to cut costs, protect margins, and at the same time reposition as digital-first businesses.

Telcos have responded to those expectations by experimenting with multiple AI use cases such as customer service, network operations, productivity and more. NVIDIA reports strong uptake: 97 percent of surveyed mobile operators are now adopting or assessing AI in their operations.

However, there is a growing AI maturity gap between telco leaders and laggards. Telcos with high AI maturity are achieving real business results while some laggards struggle to get buy-in for new AI projects after being disappointed by initial project results.

To understand how to close this maturity gap, it helps to see the value that telcos and telco leaders have been able to uncover before going towards the various AI maturity pillars that telcos should focus on.

AI Has Been Improving Telco Value Creation and Operational Efficiency

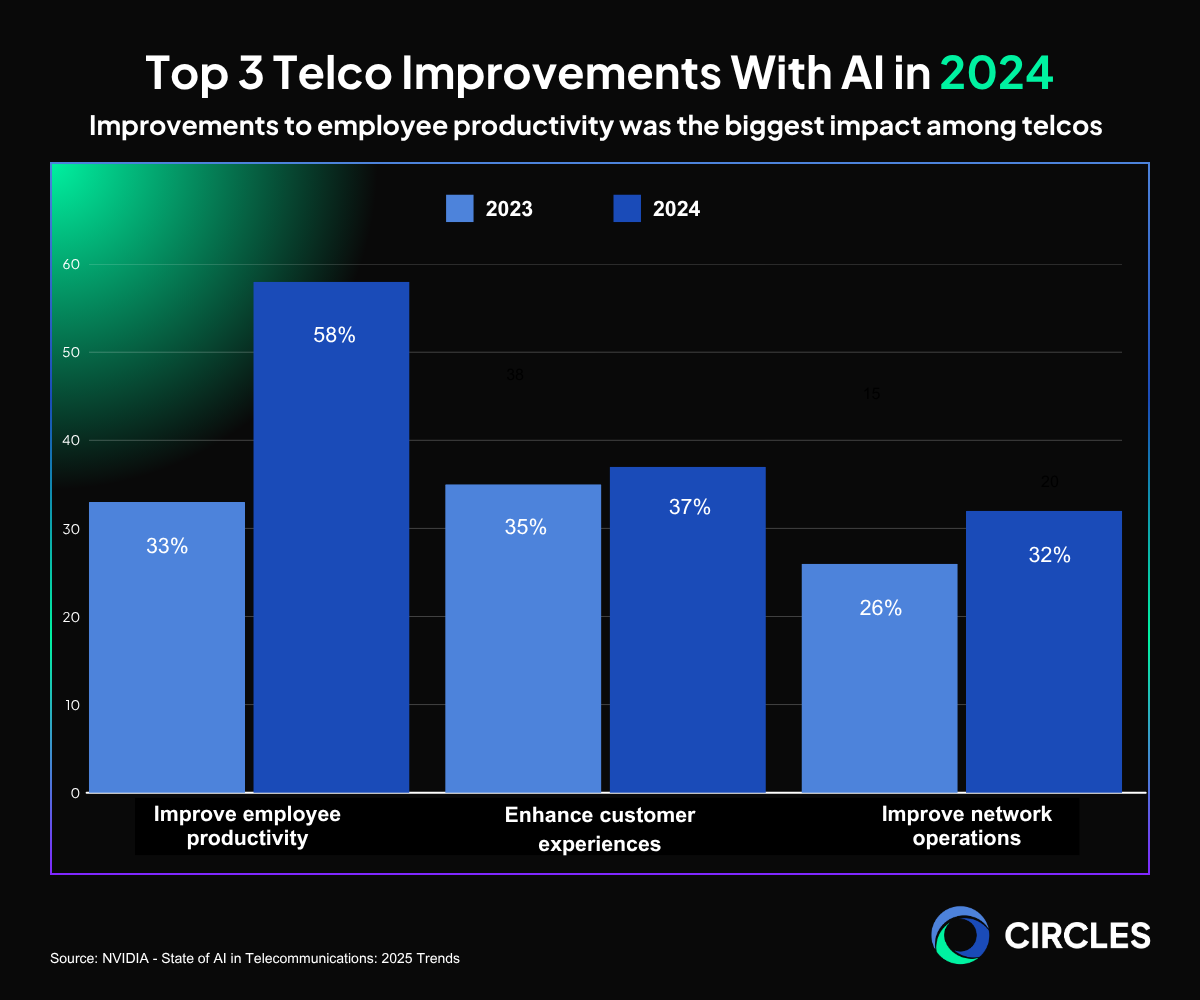

Early AI programs in telecoms primarily focused on efficiency gains and cost reductions. These include improvements to employee productivity like greater customer service agent efficiency and faster coding from IT teams. Use cases like fraud detection can reduce financial losses while network operations optimization can minimize network downtime and operations expenses.

BCG and The Community for Telecom Professionals (ETIS’s) survey in 2023 found that 58 percent of their European telco respondents saying their telco is expecting or has realized increased efficiency and productivity from their AI and Generative AI projects.1

This report mentioned that telco respondents have implemented at scale use cases like field network operations force labor optimization, smart energy savings, and network anomaly and fault detection in terms of network and operations. In terms of digital, data, and IT their engineers now use AI to generate preliminary code, automate DevOps and ML Ops while AI is also used to optimize their IT field operations work.

NVIDIA’s 2024 telco industry-wide study echoes the pattern of improved employee productivity being a main benefit, with 58 percent of respondents citing it as their biggest benefit of AI adoption. That year, 37 percent also mentioned that their AI projects yielded enhanced customer experiences.2

Telco leaders have been able to gain various measurable positive business results from their AI projects:

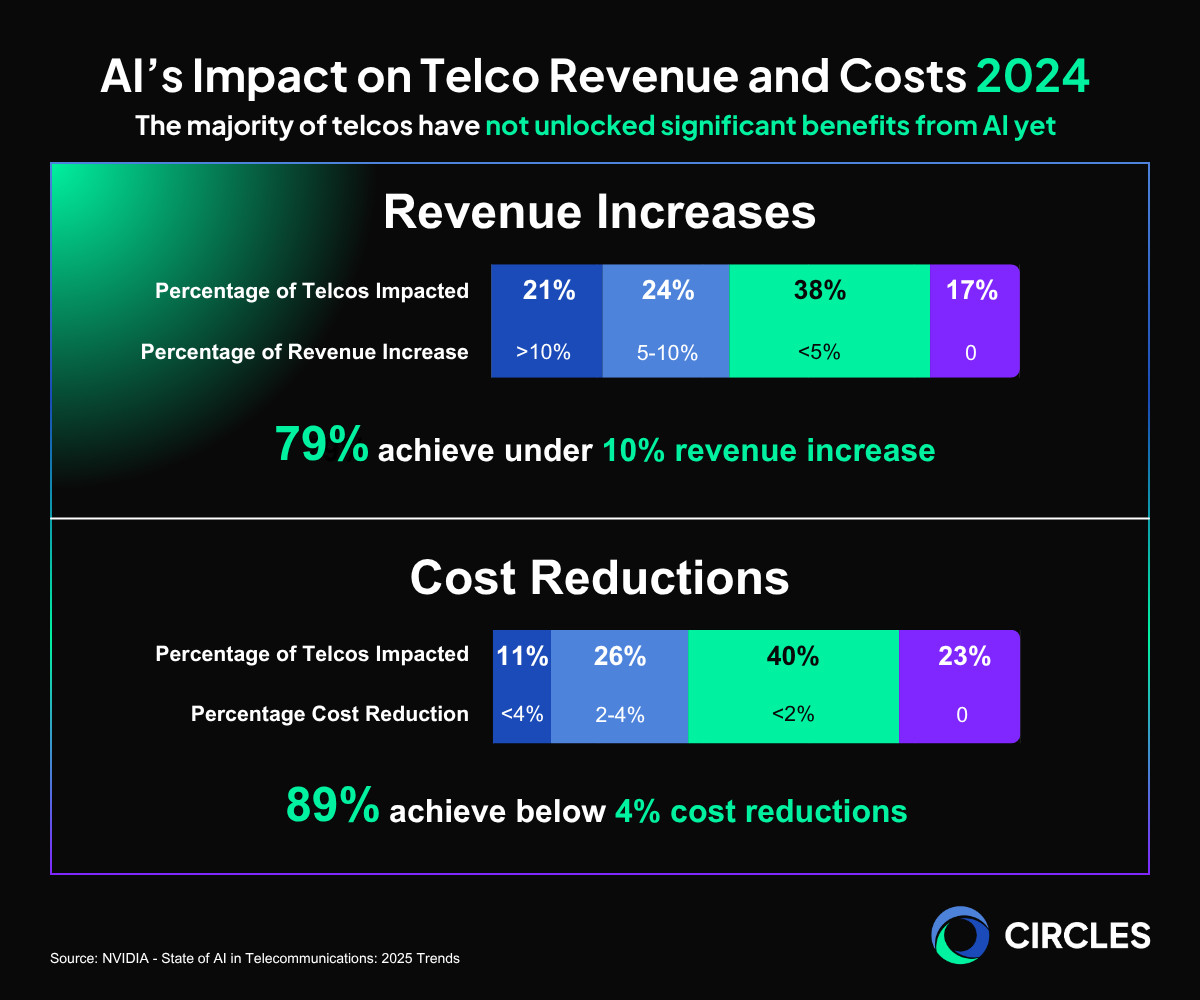

While these results are encouraging, there are also many telcos that struggle to get this level of success. In 2024, 79 percent of telcos achieved below 10 percent revenue increases and 89 percent achieved below 4 percent cost reductions. That’s why it’s important to close the AI maturity gap.2

AI Maturity: An Industry Still in Transition

While 97 percent of telcos are planning to or are already implementing AI,2 maturity challenges remain widespread. TM Forum reports that 60 percent of operators are stuck at the proof-of-concept stage, and only 14 percent have more than ten use cases in production.8 Some operators are scaling AI across multiple functions, while others are still stuck in proofs of concept.

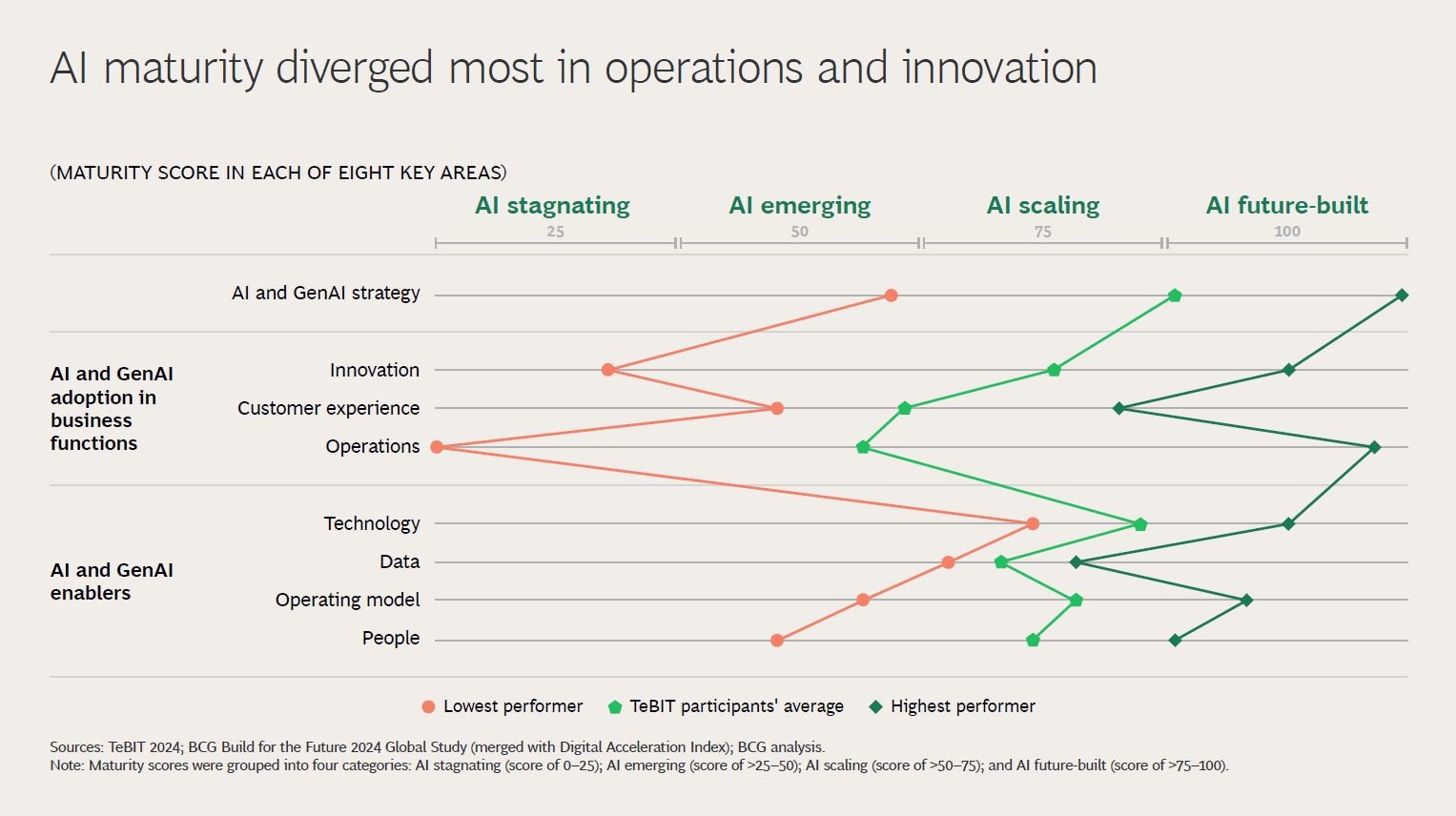

Averages Hide Stark Differences

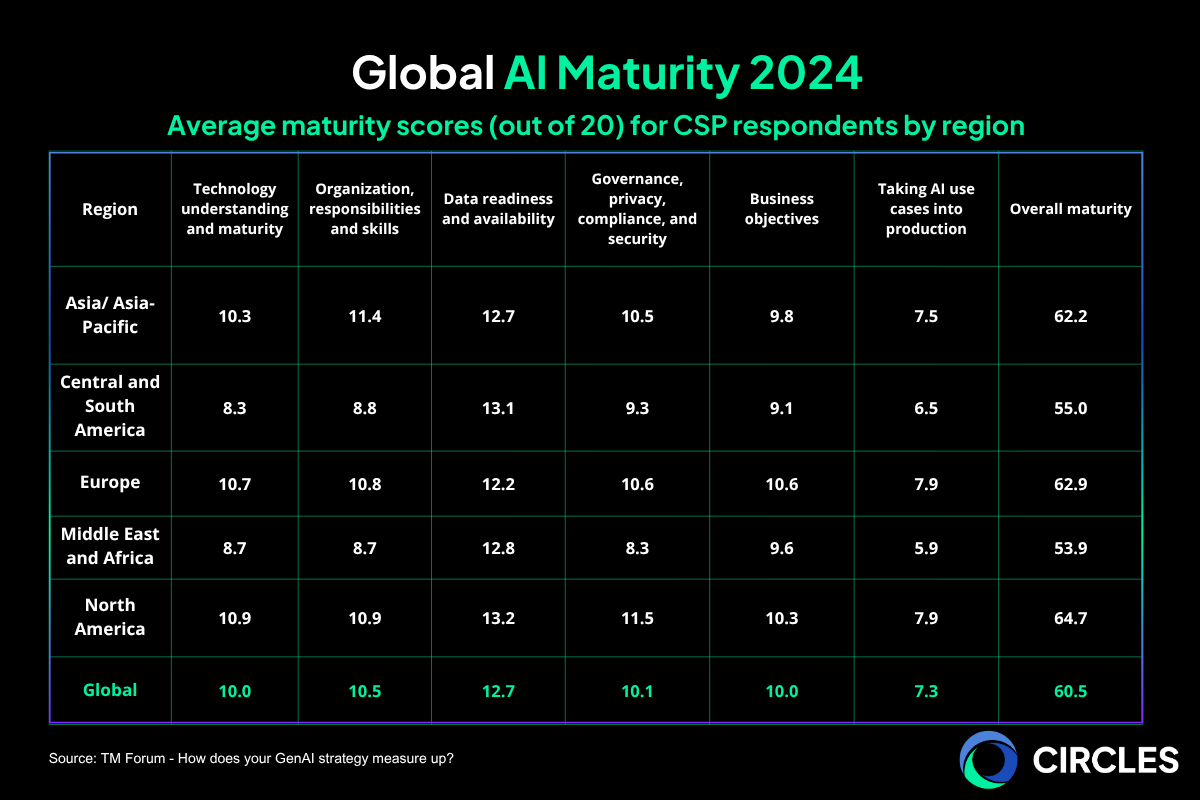

The global telco average maturity score is 60.5 out of 120, according to TM Forum’s Generative AI Maturity Interactive Tool (GAMIT).8 This comes with a wide spread where the highest individual score recorded was 116 while the lowest ten telcos scored under 20. This score was rated across six pillars:

Here are some of the top contenders that TM Forum highlighted, all of whom scored 100 or above:

When geographical differences are brought in, this divergence shows structural differences too. North America leads (64.7), thanks to the scale of its operators and proximity to hyperscalers. Europe follows with an average score of 62.9, with several incumbents building formal AI programs. Asia is polarized: giants in China, India, South Korea, and Japan are global frontrunners, while smaller regional players lag far behind.

This graph from 2023’s BCG TeBIT also shows a large disparity between telco leaders and laggards in terms of AI implementation in Europe. The biggest gaps are in operations and innovation between leaders and laggards.

To better understand how laggards can catch up with AI mature telco leaders, the following section breaks down TM Forum’s six AI maturity pillars and their findings.

Pillar 1: Technology Understanding And Maturity

Most operators are still learning the fundamentals.

78 percent mentioned that they are at the early stages of being able to get the most accurate results for different use cases. Many are still in the early stages of mastering techniques like retrieval-augmented generation (RAG), prompt engineering, and fine-tuning.8

85 percent are not yet able to make decent assessments of the cost and ROI of using different AI techniques for different use cases.

Meanwhile, more mature operators have built their own platforms, which lets internal users choose between different LLMs while providing recommendations on which LLMs provide the best results at the lowest cost.

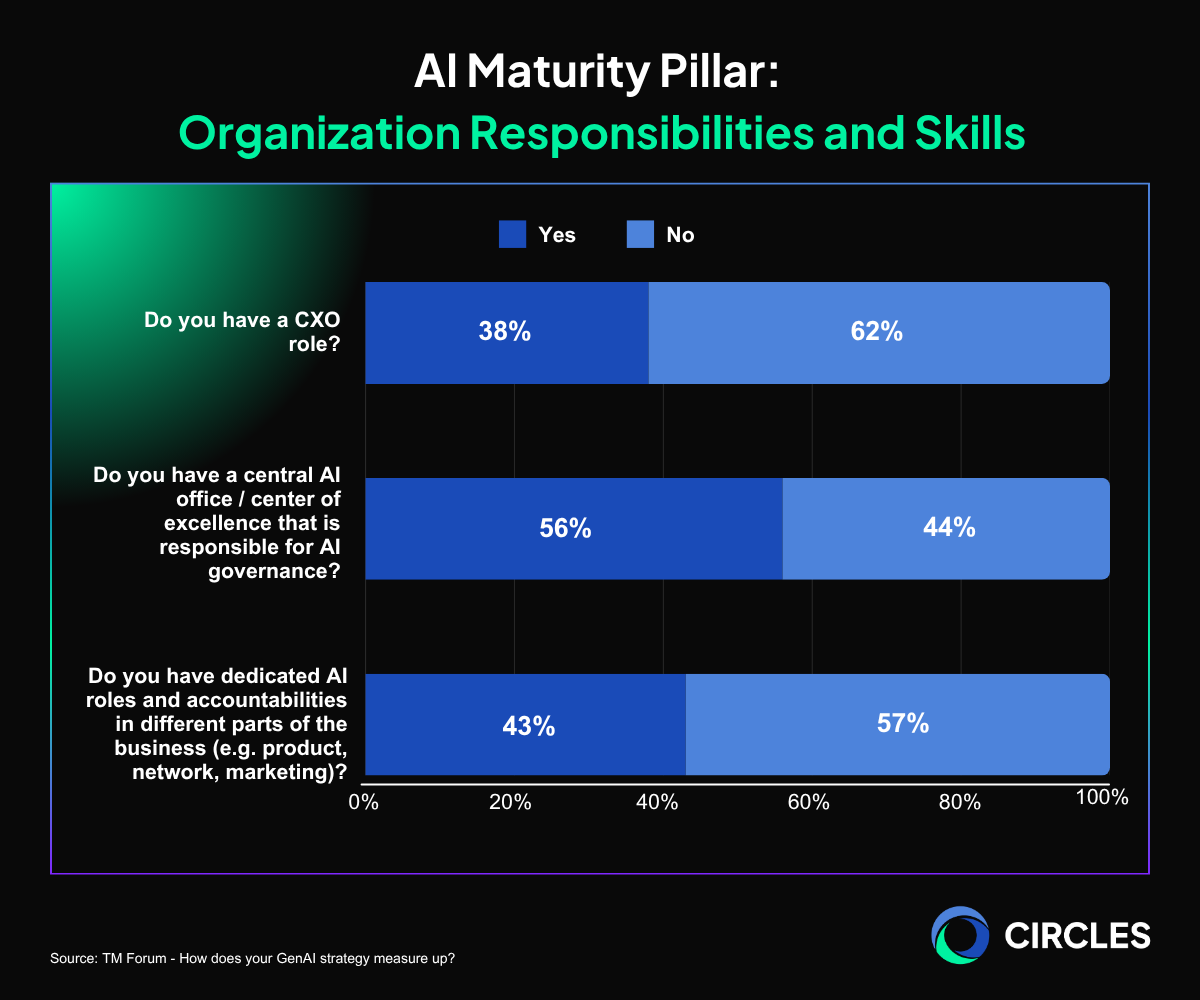

Pillar 2: Organization, Responsibilities, And Skills

Having the right talent is good, but not having organizational structures that can support them can also become a critical bottleneck. 38 percent of telcos have a C-level executive with AI as a primary responsibility. This marks a change in how telcos are approaching AI as previously telcos would place AI responsibilities under the CIO or as part of a digital team or business unit.

56 percent have established a central AI office or center of excellence. Centralized functions like these are key for making company-wide rules, guidelines, and technology platforms that let teams apply AI to various use cases.

Roughly one in three have begun skilling multiple teams in AI, but even the most mature players continue to recruit aggressively.8

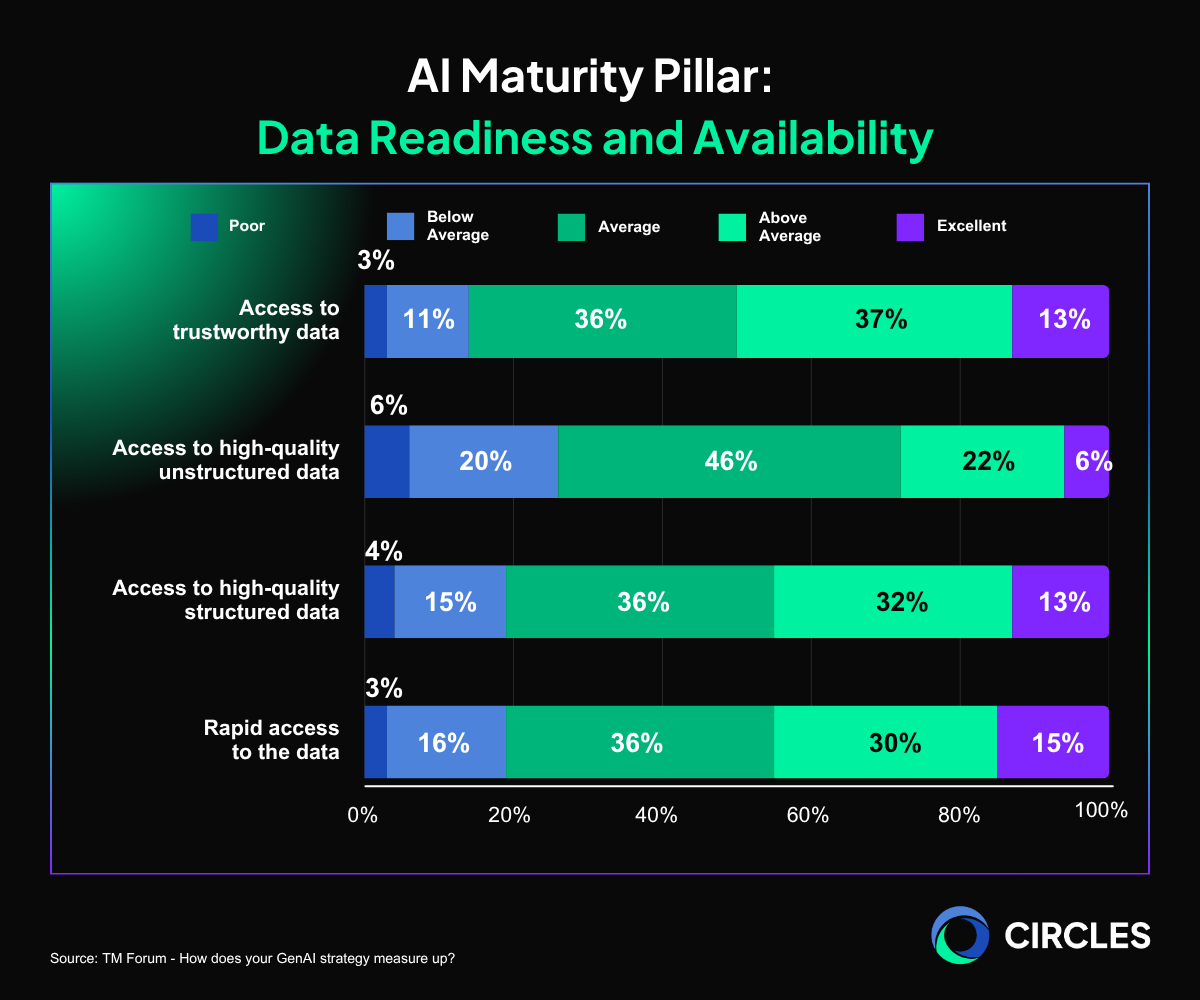

Pillar 3: Data Readiness

In order to deploy GenAI effectively, telcos need to get their data AI-ready. Data quality is improving, but silos remain the telco industry’s Achilles’ heel. Many GenAI use cases need access to high quality data, and mature operators have noted that deploying AI at scale needs a newer, better level of data sophistication and democratization. Telcos currently rated themselves as follows:8

The telco industry as a result continues to battle against these challenges: breaking down data silos, building platforms that make data easy to access and easy to use, and making new data sets, including unstructured data.

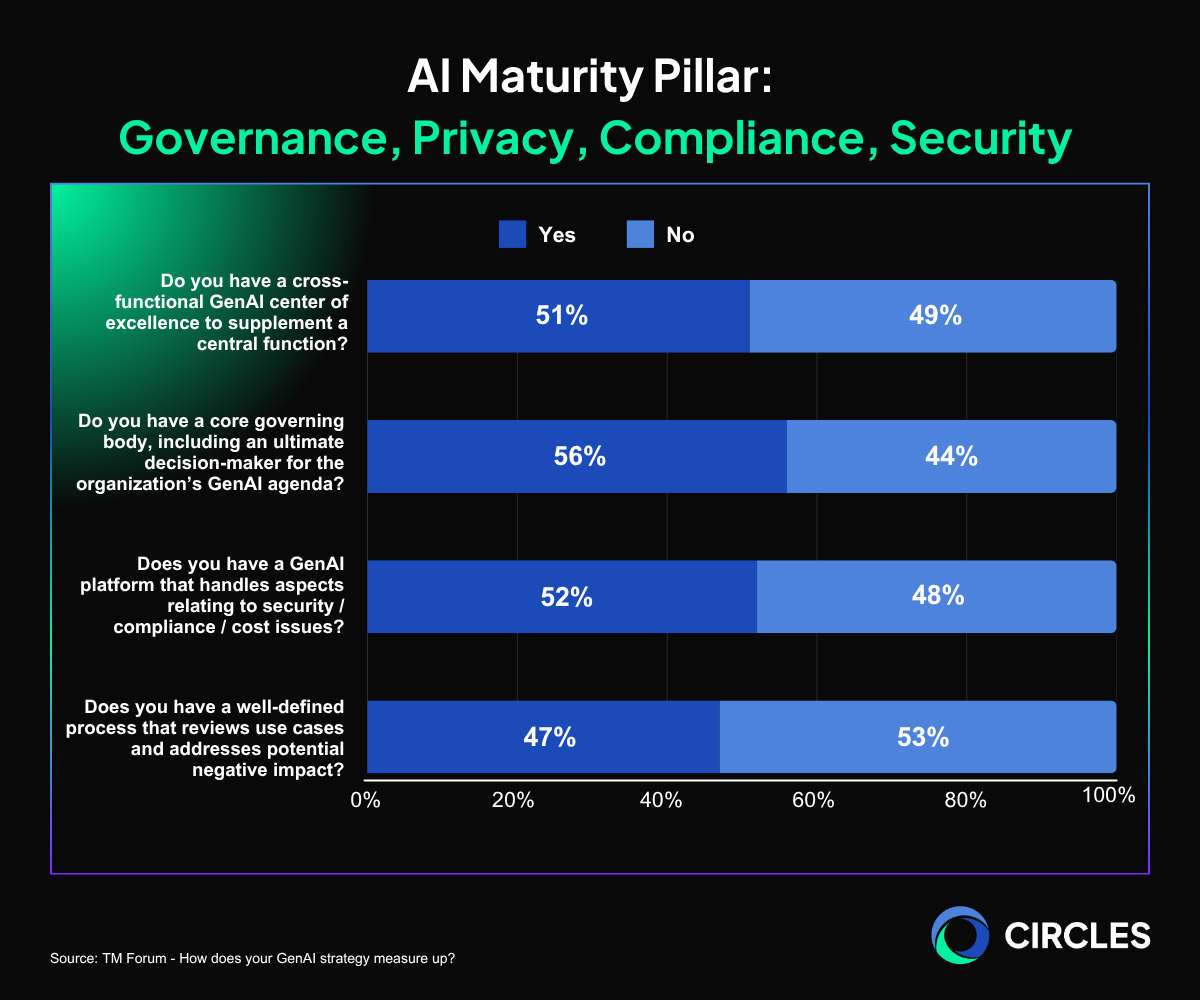

Pillar 4: Governance, Privacy, Compliance, and Security

About half of TM Forum’s respondents mentioned that they have infrastructure in place for governance, privacy, compliance, and security. These structures need to be chaired by knowledgeable experts who can enable the telco to make rapid and effective AI-related decisions.8

In some cases telcos may already have governance systems in place for AI and data which can be updated for Generative AI while other telcos have designed their governance systems from scratch.

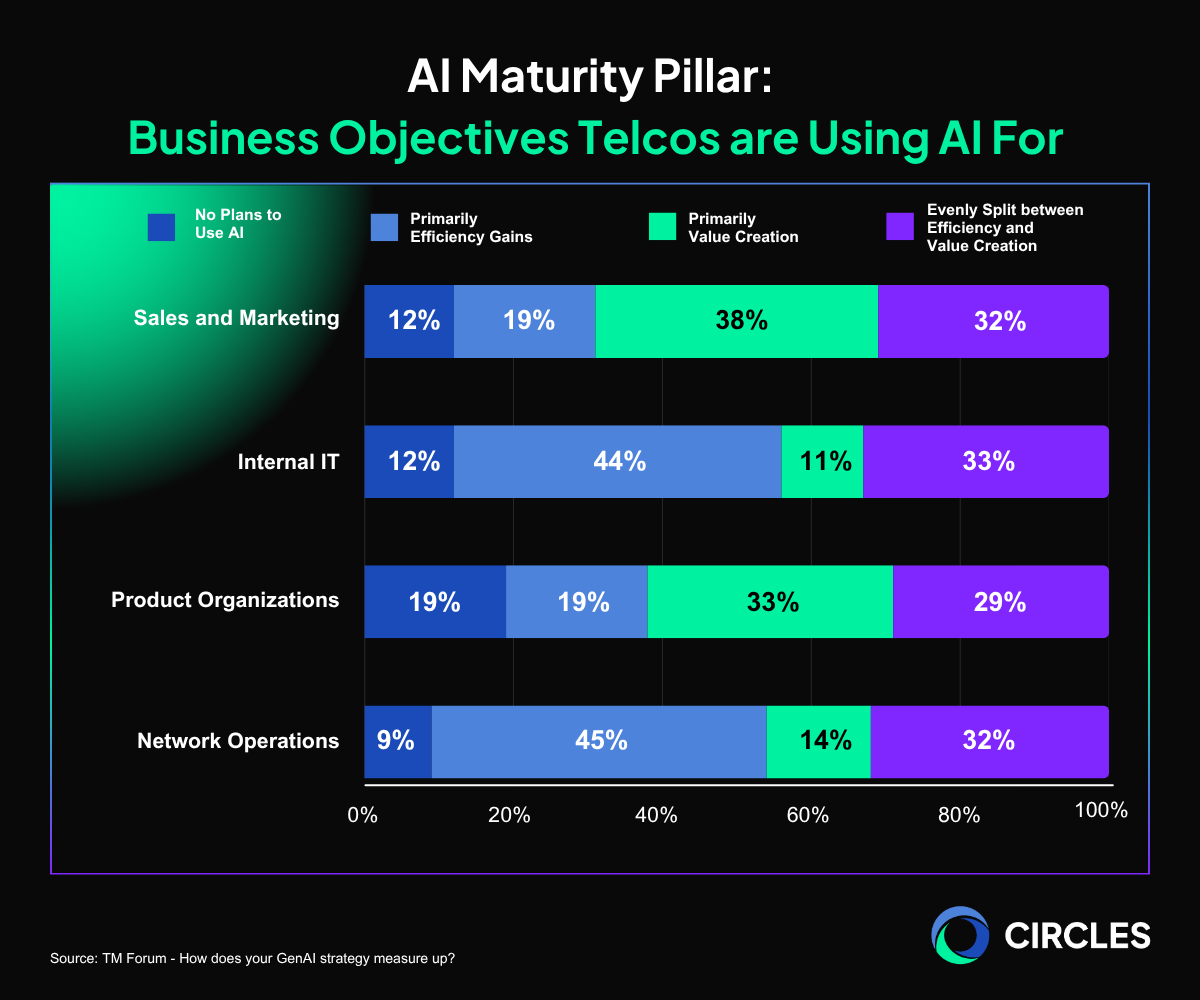

Pillar 5: Business Objectives

There are signs of greater maturity in intent. Previously, many telcos would consider the business value of tech upgrades, such as upgrades to BSS software in pure cost saving terms. Today, roughly a third of telcos report splitting the business objectives of AI projects evenly between efficiency and value creation for different functions.

In terms of AI projects that are being put into production, telcos have been heavily focusing on chatbots and other internal use cases.

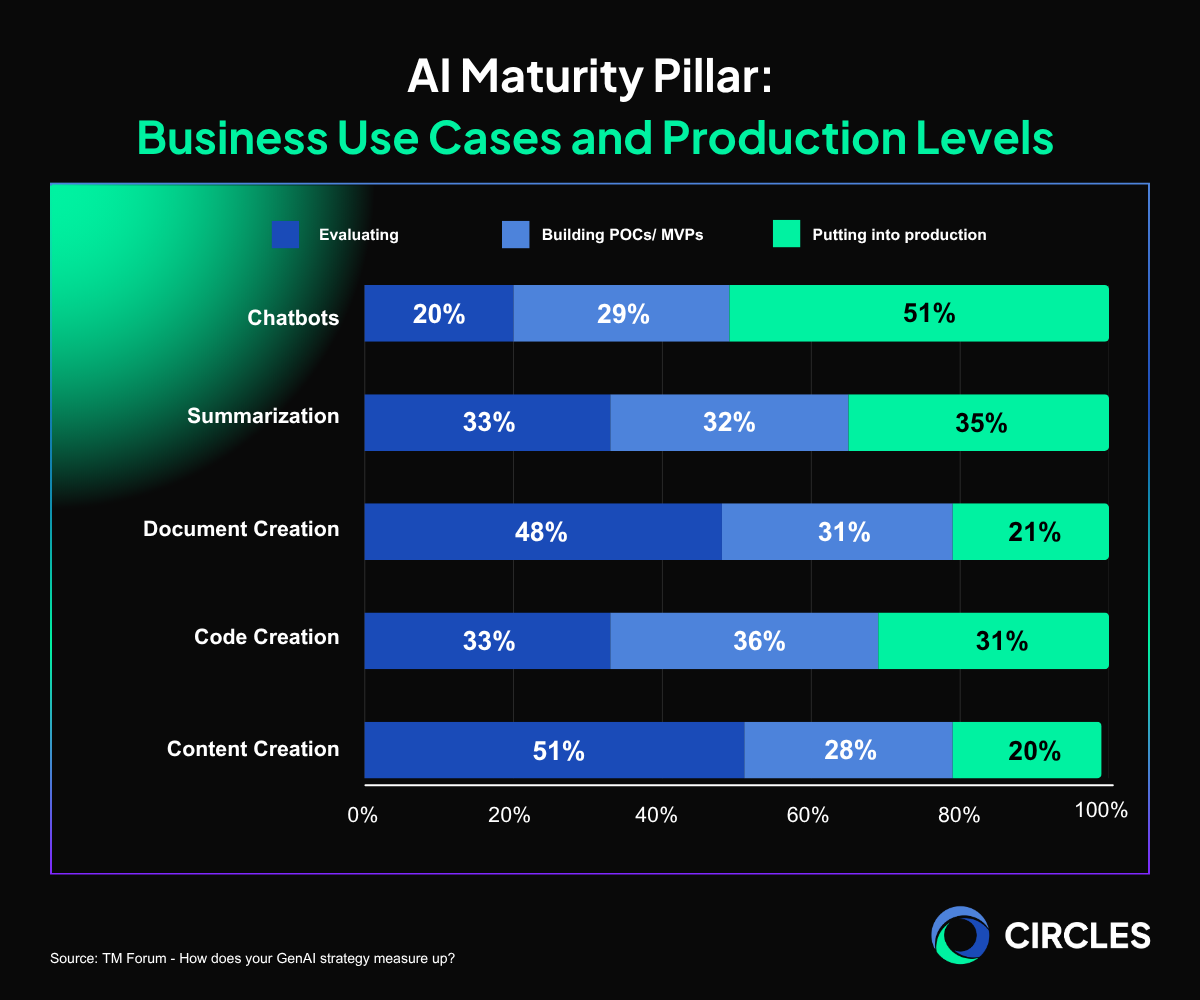

Pillar 6: Taking AI Use Cases Into Production

Scaling remains a weak link. 60 percent of operators are stuck at the proof-of-concept stage or earlier, and only 14 percent have more than ten GenAI use cases in production. Many were disappointed by initial outcomes, dampening enthusiasm for further rollouts.

The number of GenAI use cases that telcos are launching further highlights the gap between leaders and laggards: the number of use cases range from zero (26 percent of respondents) to more than 10 (14 percent of respondents).

In summary, telcos vary wildly in terms of AI maturity. While some are leading the industry in terms of almost every AI maturity pillar, many others lack the ability to systematically test, select, and fine-tune the most cost-effective large language models for specific business needs.

Leapfrogging the AI Maturity Race

These benchmarks show that there are no clear winners in the telco AI maturity race but there is an emerging gap between leaders and laggards. Fortunately, as digital industries like video streaming subscription services have shown, competitors have methods of rapidly catching up.

Telcos can close data readiness, technology, and governance and talent gaps by working with the right partners who can co-develop solutions that drive towards their AI-enabled telco vision.

Partners like Circles have been working with various global partners to keep their telco brands AI-enabled and cutting edge. Circles is pioneering the transformation of telecom into an Anticipatory Techco with its groundbreaking AI Digital Mobile Operator (AI-DMO) model.

By fusing AI, data intelligence, and deep 360° consumer insights, Circles helps telcos unlock new revenue streams, achieve cost savings, boost NPS, and build innovative business models.

Circles’ AI stack is designed by operators for operators, ensuring relevance, speed, and scalability. Validated through deployments with global leaders such as Telkomsel, AT&T, and KDDI, the platform leverages multi-market learnings to deliver proven results. You can find out more about how partners can help to close the AI maturity gap in this article.

If you are looking for a partner to help you catch up with AI mature telco leaders, contact us today or sign up for a demo below:

References:

- TeBIT 2024 Report: Smart AI Usage for Telcos | BCG

- NVIDIA - State of AI in Telecommunications: 2025 Trends

- Meet SuperTOBI - Vodafone’s new Generative AI virtual assistant now serving customers in multiple countries

- Verizon uses GenAI to improve loyalty | Reuters

- 5 AI Case Studies in Customer Service and Support | VKTR

- AT&T Transformed into an AI Company with H2O.ai

- SK Telecom Unveils ‘Aster(A*),’ Its New Global AI Personal Agent at SK AI Summit 2024

- TM Forum - How does your GenAI strategy measure up? Key findings from our Generative AI Maturity Interactive Tool